Philip H. Dybvig

Washington University in Saint Louis

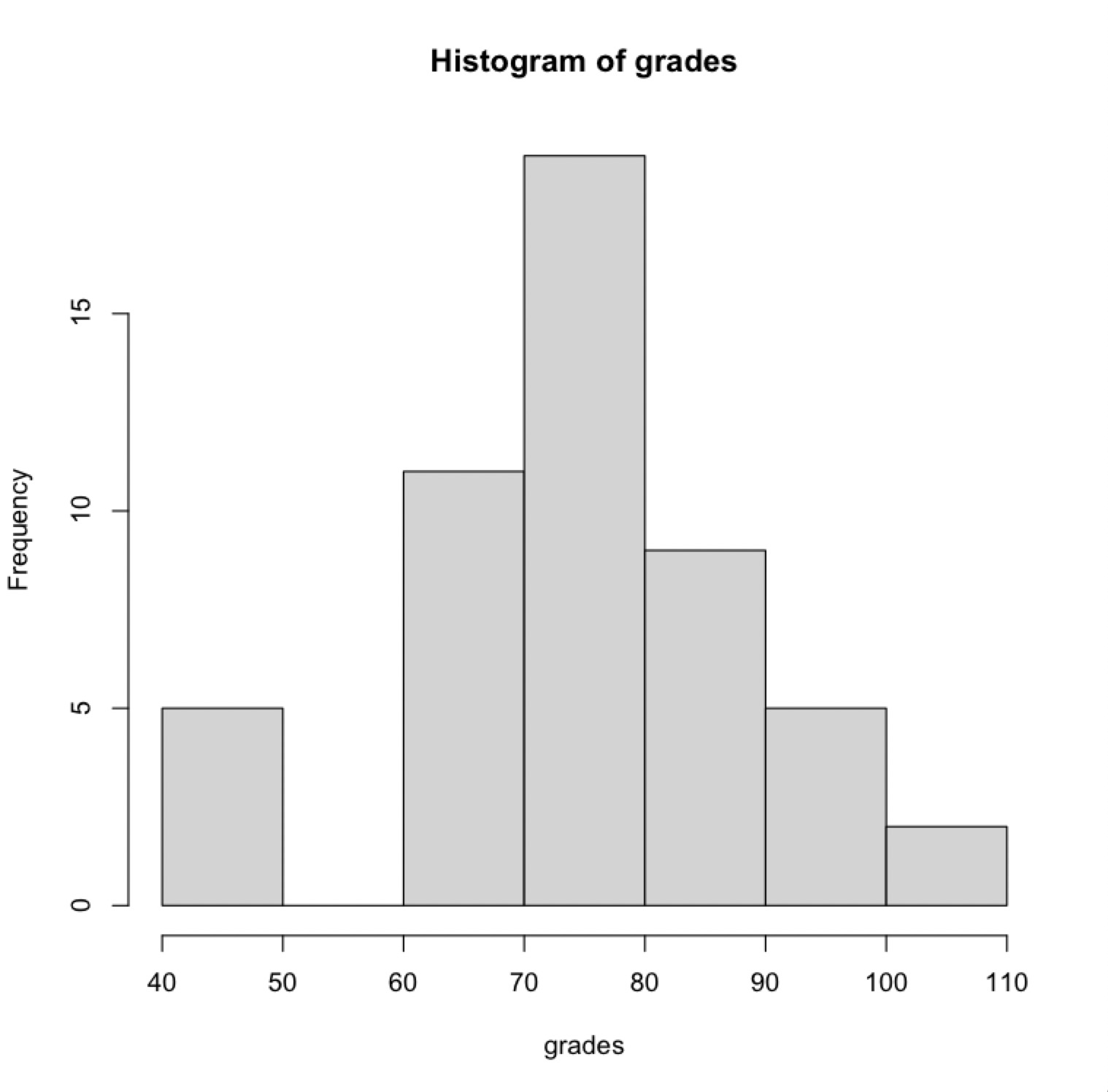

Final exam results: there was a large dispersion in the exam results:

Coming to the end of the class!

This may not affect anyone in this section, but in Saint Louis, Daylight Savings Time starts early AM on March 14 (Saint Louis time). After this time, Beijing time will be 13 hours ahead of Saint Louis, not 14 hours. This does not affect the TA section this week (which is on March 13, Saint Louis time), but it does affect the two remaining classes and the final exam.

TA session The final TA session, discussing Homework 5, will be held Saturday, March 13 at 7:00PM CST (Sunday, March 14 at 9:00AM Beijing Time Zone)

Monday class will continue our discussion of the one-shot approach. March 15 at 1:00PM CDT (Tuesday, March 16 at 2:00AM Beijing Time Zone)

Wednesday class discussing Homework 6 + Xtreme review for the exam. March 17 at 1:00PM CDT (Thursday, March 18 at 2:00AM Beijing Time Zone)

Final Exam The final exam will be held on Saturday, March 20, 8:00PM-10:00PM Saint Louis time, which is Sunday, March 21, 9:00AM-11:00AM Beijing time. Here is a description of what you are expected to know on the final exam: howtofinal.pdf. We have covered a lot of material, and you probably want to know what may be on the exam and what will not be covered.

Important: Exam Rules This is a closed-book exam with absolutely no electronics allowed outside the Zoom interface, which must have camera on, and for submitting the exam. For the exam, you are not permitted to have access to notes or any electronics, including cell phones, computers, mp3 players, iPads etc. All of these devices are computers that can be used to store information that can give an unfair advantage and most allow communications which also could be used for cheating. I want to make sure there is not even an appearance of cheating. Please take care to follow these rules. I don't like reporting infractions, but it is my duty and you will not be happy if I have to report you.

Welcome to Mathematical Finance! We will cover some interesting mathematical tools that are very useful in practice, with a focus on applications to investments.

This section is available in-person and on-line. Class meetings will be held in Zoom. Information on the Zoom meetings can be found in the course's Canvas page. The classes will also be recorded, with recordings available on Zoom. Some more information is available in Lecture 0 below and in the syllabus.

Homeworks Here are homeworks you can work to help to learn the material. Although they will not be graded, I urge you to work the homeworks before the TA session when they will be discussed.

Homework 1 answers to be discussed by the TAs on Saturday, February 6 at 7:00PM CST (Sunday, February 7 at 9:00AM Beijing Time Zone)

Homework 2 answers to be discussed by the TAs on Saturday, February 13 at 7:00PM CST (Sunday, February 14 at 9:00AM Beijing Time Zone)

Homework 3 answers to be discussed by the TAs on Saturday, February 20 at 7:00PM CST (Sunday, February 21 at 9:00AM Beijing Time Zone)

Homework 4 answers to be discussed by the TAs on Saturday, March 6 at 7:00PM CST (Sunday, March 7 at 9:00AM Beijing Time Zone)

Homework 5 answers to be discussed by the TAs on Saturday, March 13 at 7:00PM CST (Sunday, March 14 at 9:00AM Beijing Time Zone)

Homework 6 answers to be discussed by me in class on Wednesday.

Slides Most of the lectures will use a virtual whiteboard. This is a good format for technical material, and this is also what my TAs suggested. However, I am developing a set of slides for your use as supplemental material.

Lecture 1: Decision theory and static choice problems

Lecture 2: Dynamic programming

Lecture 3: Multiple assets, hedging state variables, and pricing models

Lecture 4: FTAP, valuation, and the one-shot approach

I suggest the following book chapter for background readings on single-period models:

Download Dybvig, Philip H. and Stephen A. Ross (2003), Arbitrage, State Prices, and Portfolio Theory, in George Constantinides and René Stulz, ed., Handbook of the Economics of Finance, volume 1b, North-Holland.

There is no textbook for the class, and the class is designed to be self-contained. If you want a textbook for an alternative exposition and coverage of more topics, I recommend the following book:

Back, Kerry, 2017, Asset Pricing and Portfolio Choice Theory, second edition, Oxford University Press.

Kerry is a serious scholar and my co-author. He was formerly at Washington University, but he has moved to Rice University.