Adjusting for inflation: real returns

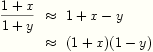

Having your portfolio value in dollars increase by 10% does not leave you any better if there is inflation and the spending power of a dollar falls by 10% at the same time. If we have an inflation rate of 5% in a year, then it takes 5% more dollars to buy the same goods. In terms of spending power, we have that the value of your holding in an asset increases by a factor

where  is the

inflation rate over the same period as the return. The final

approximation is due to the mathematical fact that

is the

inflation rate over the same period as the return. The final

approximation is due to the mathematical fact that

when  and

and  are close to zero. This tells us

that ignoring compounding (interest on interest) is not so

important over short periods.

are close to zero. This tells us

that ignoring compounding (interest on interest) is not so

important over short periods.

Phil Dybvig

|

Inflation over a period is the percentage increase in the amount of money required to purchase the same bundle of goods. The part of any increase in asset value equal to inflation is illusory. While returns in currency units, called nominal returns, are relevant when we are funding known dollar obligations, it is more common that we should be interested in real returns that have been adjusted for inflation. |

|

|

Periods of high inflation can deceive people who are living off their savings. Because interest rates tend to be high when inflation is high, people tend to increase consumption in these times, since they can increase spending and still preserve their savings in nominal terms. However, because of inflation, they would have to increase their savings in nominal terms to maintain the same spending power in real terms. |