Security returns

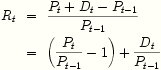

The rate of return on a security is the natural extension of the notion of an interest rate to securities with randomness. The rate of return over some time period is the change in value divided by the value at the start of the period. For example, for a stock paying a dividend, the rate of return is

In the last expression, the first term is the capital gain (loss), and the second term is the income. The rate of return is often stated in percent (also called points), or in basis points (100 basis points = 1 percent). The obvious adjustment is made for stock splits or other distributions. (Useful term: the ex-dividend day is the first day the stock trades without a claim to the dividend.)

notation:  -rate of

return

-rate of

return  -price

-price  -dividend

-dividend  -time

-time

Phil Dybvig

|

Quantifying investment performance is the first step in the scientific study of investments. The rate of return is a measure of the performance of an investment that is comparable for investments of different scales. Returns also remain comparable in the presence such events as cash dividends, share dividends, coupons, splits, and rights offerings. |

|

|

You should be warned that returns are only as good as the prices used to compute them. Returns are very meaningful for common stock of large firms that are traded more-or-less continuously, but are virtually meaningless for private equity that may be priced according to a formula because there are no market price available. Having bad prices is eventually corrected over time as distributions are made, but returns appear in the wrong period, understating the correlation with other assets. I have seen presentations by consultants in which the diversification value of private equity is grossly overstated for this reason. |